Industrial rents within the Auckland market are proving to be resilient. I was surprised by this because I have seen storage reduce across the SCS client base by about 10% since January 2023 and the data I found on stats.co.nz(1) looks like the market levels are even higher.

I have not studied economics in depth but I naturally assumed the supply and demand relationship would dictate how the market would respond. On the demand side I believed because there is now less inventory this would mean less storage, and therefore the demand for warehousing would drop. On the supply side I could not see much change because it is difficult to reduce the number of warehouses. I could see over a mid to long period a reaction through the reduction in development (relative to GDP) but this would not affect the short term because industrial warehouse projects take at least 18 months execute, I know this because this is how long it took to build our Tidal Road facility in 2021, and more recently in Christchurch* we signed off on a build project several months ago that will not be delivered until Q1 2025. This long development period means projects being completed now were started around the beginning for 2022 when demand was still high. This lag is important to understand and I will come back to later.

So my underlying assumption on supply and demand must have missed variables or relationships because of the resilience we are seeing. This intrigued me so I decided to dig a bit more.

A key part of rental levels sits within the actual agreement, because of the capital required to get developments underway or to simply purchase the asset, landlords need confidence that they will have long term income to amortize the costs against. For this reason long term leases are signed off with annual reviews. The annual reviews for the most part are fixed or tied to CPI with a market review resetting the rate periodically. Market resets for the majority of leases include a “hard ratchet” mechanism which prevents the rent from decreasing or a “soft ratchet” mechanism which reduces the amount rent can reduce (eg the maximum decrease could be 5%, 10% or a tie back to the lease rate on commencement).

Knowing that leases mostly only go up (or at least hold) then I looked at how long businesses have signed up leases because effectively this has tied them into a historically set price path. The terminology landlords give this piece of data is “WALT” (weighted average lease term). WALT is a key metric for landlords because this gives them a measure that they can use around forward confidence of income streams. Two of New Zealand’s largest industrial landlords are Goodman and PFI who control about $7B worth of warehouses. Their WALT’s are 6.3 years(2) and 5.8 years(3) respectively. This explained to me why a large portion of the market is still experiencing high rents but not why new leases are being signed at high rates when the demand is reducing.

Industrial property at its core is an investment. A simple investment example is if I invest $2000 I expect an income stream of say $200 per annum. Dividing $200 by $2000 gives me 10% which is my yield. However all investments also carry a risk-reward ratio and investors use this in collaboration with the yield when deciding where they deploy their capital. Naturally when interest rates are high (like now in NZ) then the expectation is that other investments will also have higher returns otherwise the money will flow to high yielding “safe” assets like bank term deposits or bonds instead of investments like property, shares and businesses. I know when I say this, the bond markets have had a bad year and some American banks collapsed. I would need to get a financial expert involved to talk to the reason for this competently. For now I will just use the premise money will move to safer assets if the yields are the same.

When looking at industrial property the yield is created using the following formula:

Yield = Rent / (CostLand + CostMaterials + CostLabour + DevMargin)

We know the yield needs to increase because interest rates are higher now compared to a couple of years ago, we know materials and labour are higher because of inflation, we know DevMargin needs to exist otherwise Developers will not build. The math of this equation in this paradigm leads us to 3 outcomes if a new development/lease is to be executed.

- A higher rental rates is agreed,

- Land owner lowers the price of their land, or

- A combination of both

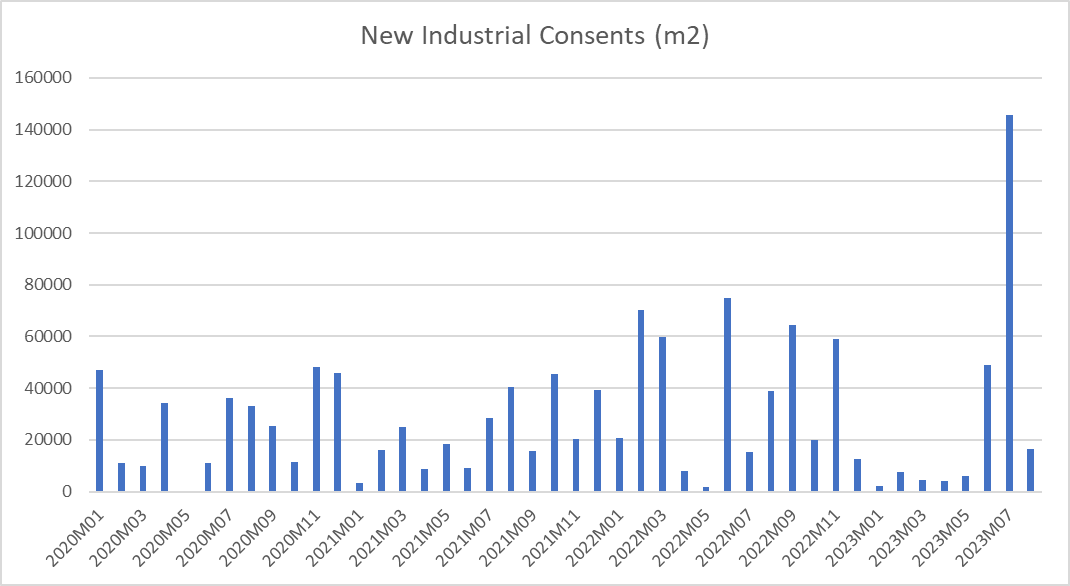

This brings me back to my comment earlier on the natural lag that developments have (circa 18 months). Leases being executed today on new developments are being executed at levels set further back than the beginning of this year when inventory levels started softening. While this is a factual outcome, the question is “are newly set development rental rates a true indicator of the market?” Time will tell. Perhaps a signal is the forward forecast of building projects being executed because developers will know the demand levels and will be supplying if it is present. Below is a graph(4) on the Auckland Industrial Consents, for the majority of this year it has been dead but recently there have been several large projects reported. There is also the risk of assuming developers are right because some developments are speculative.

So current leases are in the cycle of rent reviews set at the time of signing, new development leases are set at when the agreement against the development is made approximately 18 months ago, which leaves new leases on current assets. These leases are the most exposed to market forces.

However some things that are not always easy to spot are the structures the landlords put inside the lease. A couple of examples are:

- Operating Expenses

- SCS has several different landlords and while operating expenses are legally a pass through of cost there often is a “management fee” included. Our experience has shown this fee can vary greatly.

- Incentives

- Sometimes landlords will offer an incentive to bring you on as a tenant, this is often a “rent free period” which has monetary value and as a tenant you will work into your financial calculations. For example you might be willing to pay a higher rent in trade off for 9 months rent free up front.

- SCS has also experienced being offered cash or loans instead of rent free period.

- Rate Structure

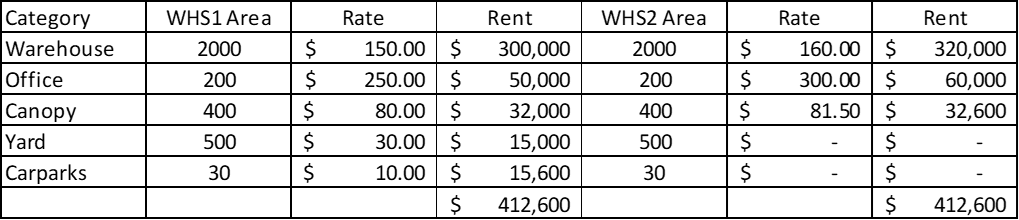

- Leases are constructed using an annualized rate against a category of area. There are many different categories such as Warehouse, Office, Canopy, Breezeway, Yard, Carparks etc. However 2 buildings next to each other, leased at the same time may have a different rate against a single category because the tenant decides they don’t want to use all of them. The trick as a tenant who moves into the suburb a month later is to know the rent level is $412.6k … not that the expected rental rate of $160/m2 is the market rate.

Summarizing this all up, I have circled back to the belief market forces around supply and demand will ultimately dictate the price. It will come down to whether the tenants can achieve passing through the rental costs to their customers. I am unsure if this will be possible, our customers are telling us the large retailers like Foodstuffs, Progressive, Farmers, Briscoes are pushing back hard because the ultimate consumers can not sustain the increased costs. If the pass through is possible then I am sure there is room to keep rates high, if not then landlords will need to compete, especially if tenants are reducing inventory which will mean an excess of warehouse space. How this plays out I am unsure of, it will be the balance of the state of the economy vs the timing of the supply and demand of industrial property which as discussed has natural lags built into the system (throttling effect of WALT and development lead times). It is my underlying belief it will get tougher before it gets better so I believe landlords do need to be strategic.

*Final note, I made reference to a Christchurch development we have just signed off. This development will cannibalize storage out of the Auckland market and is being executed to help large customers who can execute a dual DC model reduce freight costs, therefore this build supports the argument around the Auckland market demand is weakening.

References:

- https://infoshare.stats.govt.nz/SelectVariables.aspx?pxID=84132483-d272-44df-9ddd-de26d1ac3860 (Distribution Category)

- https://2023.goodmanreport.co.nz/

- https://www.propertyforindustry.co.nz/investor-centre/resultscentre/

- https://infoshare.stats.govt.nz/SelectVariables.aspx?pxID=a113131b-4ced-4593-8e6c-0378aebdccc1